Volatility Trading Terminology

ボラティリティ取引の用語

all or none (AON) - オール・オア・ナン(AON)

A buy or sell order that instructs the broker to fill the order completely or not at all.

注文の全数量を約定させるか、まったく約定させないように指示する注文方法。

Altiplano - アルティプラーノ

An exotic option based on multiple underlying assets. If none of those assets meets a specified benchmark rate of return during the option’s life, the investor receives only a pre-set coupon. If any underlying surpasses the benchmark, the investment effectively converts into vanilla options on each underlying.

複数の原資産を対象としたエキゾチック・オプションで、満期までにいずれの原資産も指定されたベンチマークのリターンを上回らなければ、投資家は所定のクーポンのみを受け取る。一方、いずれかがベンチマークを上回れば、各原資産についてバニラ型オプションに転換される形になる。

The type that can be exercised at any time up to the maturity date.

Autoregressive Conditional Heteroskedasticity. The ARCH model assumes that there is autocorrelation between the squared past error terms (or residuals) and predicts future variance (volatility).

Option contracts whose payoff depends on the average price of the underlying asset over a certain period of time.

損益が、ある期間にわたる原資産価格の平均値に基づいて決まるオプション契約。

average price option - 平均価格オプション

A type of Asian option in which the strike price is fixed and the average price of the underlying asset is is compared with the average price of the underlying asset to determine the payoff.

アジアン・オプションの一種で、あらかじめ決められた行使価格と原資産の平均価格との差額で決済されるもの。

average strike option - 平均行使価格オプション

A type of Asian option in which the average price of the underlying asset becomes the strike price.

アジアン・オプションの一種で、原資産の平均価格が権利行使価格となるもの。

The price at which someone wants to sell.

市場で売り手が提示している価格。

assignment - 割り当て

The carrying out of the obligation of the writer to fulfill the terms of an option contract.

オプションの買い手が権利を行使した場合、売り手がその要求に応える義務を果たすこと。

at-the-forward - アトザフォワード

State that the exercise price is equal to the fair value of the forward contract for the underlying asset.

The state in which the strike price is closest to the current price of the underlying asset.

automatic exercise - 自動権利行使

A procedure where the clearing house will automatically exercise an "in the money" option, typically at an option's expiration date. This protects an option holder who forgets about the date or who is unable to give instructions.

清算機関が満期日に本質的価値のある(イン・ザ・マネーの)オプションを、自動的に行使する手続き。これにより、満期日を忘れた場合や、指示を出せないホルダーも保護される。

backwardation - 逆ザヤ

When the current price of an underlying asset is higher than prices trading in the futures market.

現物価格が先物価格よりも高い状態。

An exotic option whose underlying asset is a weighted average of multiple assets grouped together in a basket.

エキゾチック・オプションの一種で、複数の資産をまとめたバスケットの加重平均を原資産とするオプション。

bear spread - ベアスプレッド

A bear spread is a vertical spread strategy used when the trader is bearish on the underlying asset.

原資産価格の下落を見込む際に用いられるバーティカルスプレッド戦略。

bear put spread - ベア・プット・スプレッド

The trader buys puts at a higher strike price and sells puts at a lower strike price. The maximum profit is achieved if the underlying asset’s price falls to or below the lower strike price, minus the net premium paid.

The price a buyer is willing to pay.

買い手が市場で提示している価格。

The middle strike price in a butterfly spread. The lower and higher strike prices are referred to as the wings.

バタフライ・スプレッドにおける中間の行使価格(蝶の胴体)。低い行使価格と高い行使価格は、ウィング(蝶の羽)と呼ばれる。

bonus share - 特別配当株

Additional shares distributed by a company to its existing shareholders for free, usually in proportion to their current holdings. Also called a bonus issue, scrip issue, or capitalization issue.

既存の株主に対し、保有株数に応じて無償で交付される追加の株式。

box - ボックス

A strategy of going long on a combo with a low strike price and shorting a combo with a high strike price. In this case, regardless of the price of the underlying, at expiration you would buy the the underlying at the lower strike price and sell it at the higher strike price.

行使価格の低いコンボをロングし、行使価格の高いコンボをショートする戦略。この場合、原資産の価格にかかわらず満期時に低い行使価格で原資産を買い、高い行使価格で原資産を売ることになる。

bull spread - ブルスプレッド

A strategy designed to profit from a moderate rise in the price of an underlying asset.

原資産価格がいくらか上昇すると見込めるときに利益を得るための戦略。

bull call spread - ブルコールスプレッド

A strategy of buying a call at a strike price and selling a call at a higher strike price.

A strategy of selling a put at a strike price and buying a put at a lower strike price.

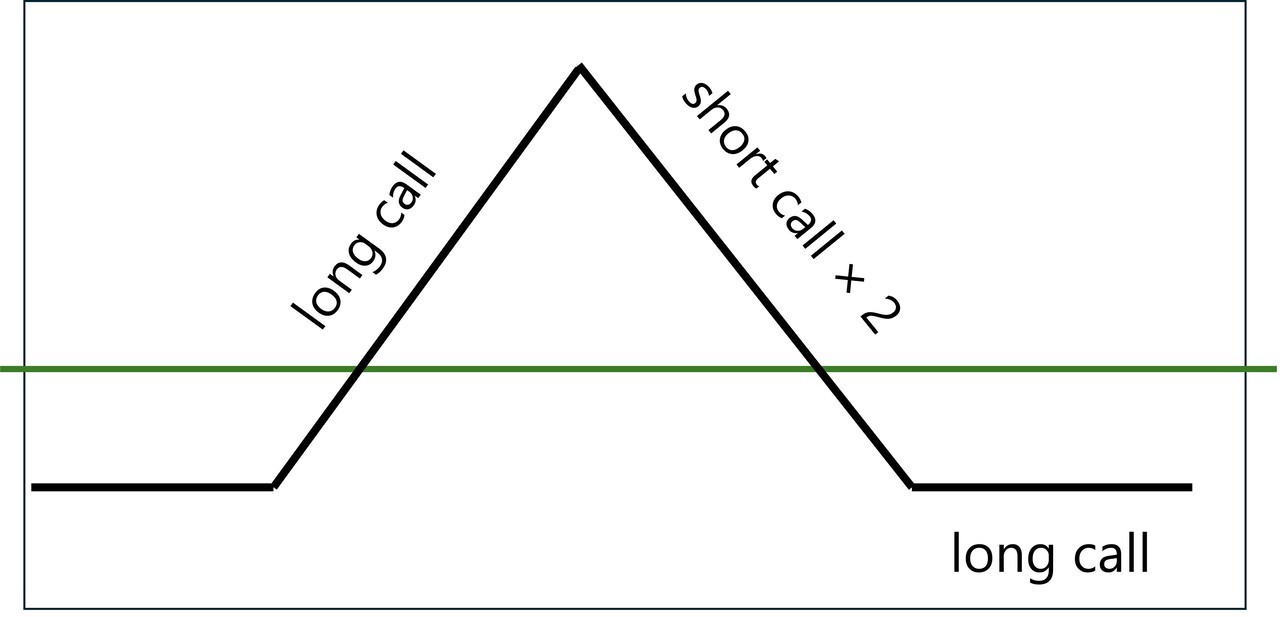

A strategy that combines options at three different strike prices, all with the same expiration date, typically involving buying one option at the lowest strike, selling two at the middle strike, and buying one at the highest strike.

満期日が同じで、行使価格が3つ異なるオプションを組み合わせて構成する戦略。通常は、最も低い行使価格のオプションを1枚購入し、中間の行使価格のオプションを2枚売却し、最も高い行使価格のオプションを1枚購入する形となる。

long call butterfly - ロングコールバタフライ

A typical long call butterfly spread involves buying one in-the-money call option with a low strike price, selling two at-the-money call options with a middle strike price, and buying one out-of-the-money call option with a high strike price. This strategy aims to profit when the underlying price stays near the middle strike.

ロングコールバタフライは、通常、イン・ザ・マネーの低い行使価格のコールを1つ買い、アット・ザ・マネーの中間の行使価格のコールを2つ売り、アウト・オブ・ザ・マネーの高い行使価格のコールを1つ買うことで構成される。原資産価格が中間の行使価格付近にとどまることで利益を狙う。

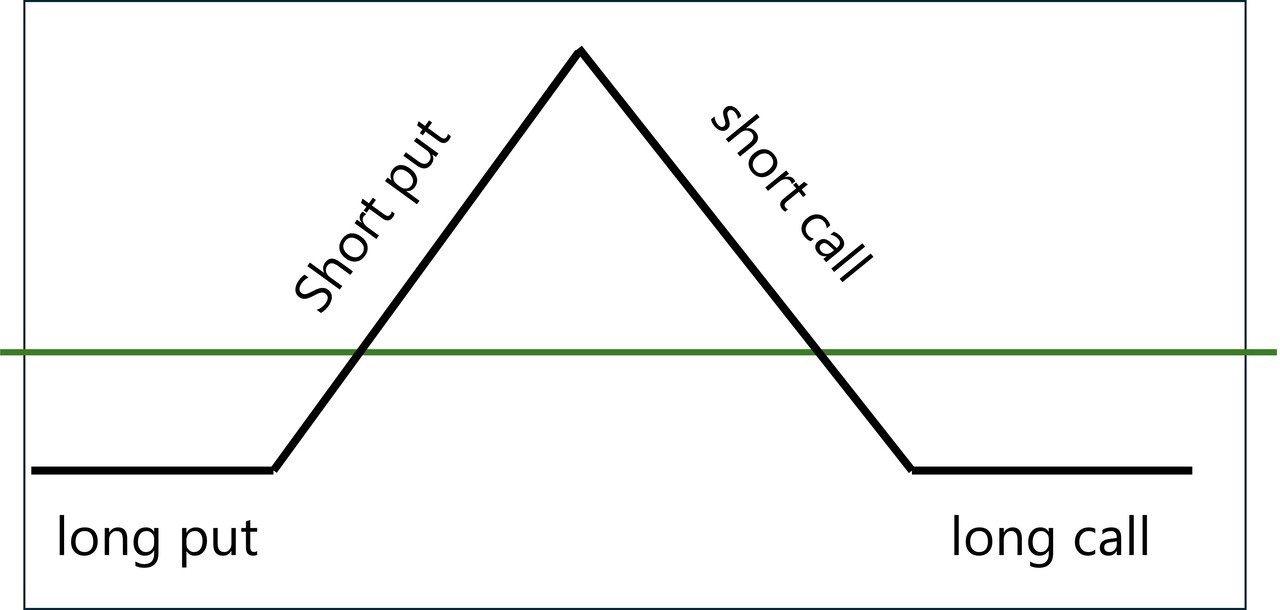

iron butterfly - アイアンバタフライ

An options strategy in which a call and a put are sold at the same strike price (the “body”), while a call with a higher strike and a put with a lower strike are purchased (the “wings”). Although the profit-loss diagram of a long iron butterfly is similar in shape to that of a long call butterfly, the iron butterfly typically starts with a net credit, since it sells the expensive at-the-money (ATM) body and buys the cheaper out-of-the-money (OTM) wings. (Whether this is referred to as 'long' or 'short' can vary depending on the naming convention used by the firm or organization.)

同じ行使価格のコール1枚とプット1枚を売る(ボディ)一方、それより高い行使価格のコール1枚と低い行使価格のプット1枚を買う(ウィング)戦略。ロングアイアンバタフライの損益図はロングコールバタフライと似ているが、ATM付近のボディを売り、OTMのウィングを買うため、通常は最初にプレミアムの差額を受け取る。(ロングかショートかの呼び方は、会社や組織によって異なる。)

A strategy to write a call option against shares you hold in the underlying. Also called "covered call," or "call overwriting."

原資産を保有し、その資産に対してコールオプションを売ることでプレミアムを得る戦略。通常はアウト・オブ・ザ・マネーのコールが用いられ、カバードコールやコール・オーバーライトとも呼ばれる。

A calendar spread typically involves buying an option and simultaneously selling another option with the same strike price but a shorter expiration date. This allows you to buy volatility from the expiration of the short-term option to the expiration of the long-term option.

一般的には、満期の近いオプションを売り、満期の遠いオプションを買う(ロング)戦略。これにより、短期オプションの満期から長期オプションの満期までのボラティリティを買う。

The right to buy an underlying asset at a certain price for a certain amount of time.

特定の原資産を特定の期間において特定の価格で購入できる権利。

carrying cost - キャリーコスト/持ち越し費用

cash settlement - 差金決済

A settlement method in which the difference between the price on the maturity date and the strike price is paid in cash, as in the case of an index option.

clearing member - 清算会員

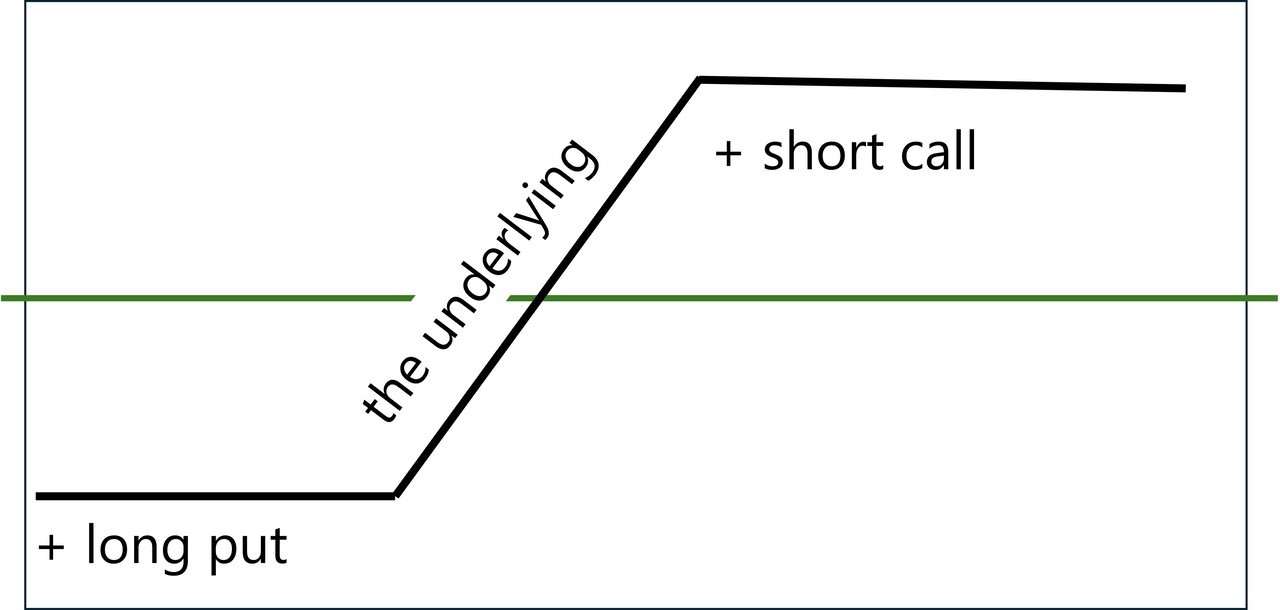

プットの買い+原資産+コールの売り

An options strategy that involves holding an underlying asset, buying an out-of-the-money put (protective put) and selling an out-of-the-money call (covered call).

原資産を保有しながら、損失を限定するためのアウト・オブ・ザ・マネーのプット(プロテクティブ・プット)を購入し、利益を制限する代わりにプレミアムを得るためにアウト・オブ・ザ・マネーのコール(カバード・コール)を売却する戦略。

Calendar collar - カレンダー・カラー

A variation of a collar strategy in which, instead of selling a long-dated (e.g., 12-month) call option, the investor sells a one-month call and rolls it over each month. This approach may help limit risk exposure in case the underlying asset's price surges significantly during the year.

カラー戦略の一種で、1年物のコール・オプションを売る代わりに、1カ月物のコールを毎月売却してロールオーバーする手法。これにより、原資産価格が年の途中で急騰した場合でも、リスクを一定程度抑制できる可能性がある。

Buying a call and selling a put with the same expiration date and strike price. It is essentially the same as buying the underlying futures contract. This strategy is employed when there is some expectation regarding dividends or interest rates.

同じ限月、同じ行使価格のコールを買い、プットを売ることで、原資産の先物を買うことと本質的に同じ。配当や金利に何らかの目論見がある場合に、この戦略をとる。

compound option - 複合オプション

contango - 順ザヤ

contract month - 限月

The specific month in which contracts are settled.

満期日の月。

contract size - コントラクトサイズ

The number of units of the underlying asset that each options contract controls, defining how much of the underlying asset you can buy or sell when exercising the option.

オプション1つに対し、権利の及ぶ原資産の数量。Shares per Contractとも言う。

conversion - コンバージョン

convexity/convex - コンベクシティ/コンベックスな

Convexity refers to the curvature in the relationship between two variables, such as an option's price and changes in the underlying asset's price. Option prices are typically convex, meaning that the price increases at an increasing rate as the underlying asset moves in the favorable direction.

オプション価格と原資産価格など、2つの変数の間の関係における曲率を「コンベクシティ」と呼ぶ。オプション価格は一般的に正のコンベクシティ(凸性)を持つ、あるいはコンベックス(下に凸)であると言われており、原資産価格が有利な方向に動くと、価格が加速度的に上昇する傾向がある。

corporate action - コーポレートアクション

Any event initiated by a company, such as the payment of dividends, stock splits, and stock buybacks, that typically affects its stock price.

通常、株式の価値に影響を与える企業の財務上の意思決定。配当、株式分割、自社株買いなど。

counterparty risk - カウンターパーティリスク

The probability that the other party in a transaction may not fulfill its part of the deal and may default on the contractual obligations.

取引相手が契約を履行しないリスク。

covered write - カバードライト

cylinder - シリンダー

deep in the money - ディープインザマネー

An option that has significant intrinsic value due to a large difference between the strike price and the underlying asset price.

deferred start option - ディファード・スタート・オプション

deliverable - デリバラブル

The underlying asset that must be delivered when an option is exercised.

Delta is commonly used to hedge an option’s exposure to the underlying asset, as it estimates how many units of the underlying asset are needed to hedge one option contract.

It is derived by taking the partial derivative of the option price with respect to the price of the underlying asset in the Black-Scholes model. Hence, delta also indicates how much the price of an option is expected to change when the price of the underlying asset moves by one unit.

Additionally, delta approximates the probability that the option will expire in the money. Generally, an at-the-money option has a delta of approximately 0.5 for calls or -0.5 for puts.

In the case of volatility futures, delta represents how sensitive the futures price is to changes in the underlying volatility index (such as the VIX).

オプションの原資産に対するエクスポージャーをヘッジするためによく用いられ、1つのオプション契約をヘッジするのに必要な原資産の数量を推定する指標。

ブラック=ショールズ・モデルにおいて、オプション価格を原資産価格で偏微分することで求められる。したがって、デルタは原資産価格が1単位動いたときに、オプション価格がどれくらい変動するかを示す。

さらに、デルタはオプションがイン・ザ・マネーで満期を迎える確率のおおよその目安ともなる。一般的に、アット・ザ・マネーのオプションのデルタは、コールで約0.5、プットで約-0.5となる。

ボラティリティ先物の場合、デルタは先物価格が原資産であるボラティリティ指数(例えばVIX)の変化に対してどの程度感応するかを表す。

delta hedging - デルタヘッジ

A method used by volatility investors to eliminate exposure to the directional movement of the underlying asset by holding a position in the underlying equal in size and opposite in direction to the option’s delta.

ボラティリティ投資家が、オプションのデルタと等しい大きさで逆方向の原資産ポジションを持つことで、原資産の方向性リスクを取り除く手法。

delta neutral - デルタニュートラル

diagonal spread - ダイアゴナルスプレッド

A strategy involving the simultaneous buying and selling of call options (or put options) on the same underlying asset, with different expiration dates and different strike prices.

満期日と行使価格が異なる、同一の原資産に対する同じタイプのオプション(コールまたはプット)の買いと売りを組み合わせた戦略。

Digital option - デジタル・オプション

A type of option that pays a predetermined fixed amount if it expires in the money. Unlike a vanilla option, the payoff does not depend on how far the underlying price is from the strike price. It is also called a "binary option."

満期時にイン・ザ・マネーであれば、あらかじめ定められた一定額が支払われるオプションの一種。バニラオプションとは異なり、原資産価格と行使価格の差額の大きさは支払額に影響しない。「バイナリー・オプション」とも呼ばれる。

discount rate - ディスカウントレート

The rate used to determine the present value of future cash flows. In options pricing, the risk-free interest rate is typically used as the discount rate.

将来のキャッシュフローを現在価値に割り引く際に用いる利率。オプション価格の計算では、無リスク金利が割引率として用いられることが多い。

dispersion trade - ディスパージョン取引

A dispersion trade is a market-neutral strategy that typically takes long positions in options on individual underlyings and short positions in a related index option. This strategy works because individual underlyings tend to have offsetting price movements, making the sum of volatility higher than that of a basket of the underlyings.

マーケット・ニュートラルな取引で、通常、個別原資産のオプションにロング、関連するインデックスのオプションにショートのポジションを取る。個別原資産の価格変動が互いに打ち消し合うところがあるため、個別原資産のボラティリティの総和がインデックスのボラティリティよりも高くなりやすいことを利用する。

drift - ドリフト

The expected average directional change in the underlying asset price.

原資産価格の期待される平均的な変化。

dynamic hedge - ダイナミックヘッジ

A dynamic hedge involves continuously adjusting the position in the underlying asset to maintain a desired risk profile and offset exposure from an option position.

early exercise - 早期行使

The act of exercising an American-style option before its expiration date.

elasticity - 弾力性

The percentage change in an option’s value compared to the percentage change in the price of the underlying asset. Also called Lambda. Delta reflects absolute changes in value, while Lambda reflects the corresponding percentage changes.

原資産価格の変化率に対するオプション価値の変化率を示す指標。ラムダ(λ)とも呼ばれる。デルタは価値の絶対的な変化を、ラムダは相対的な(割合の)変化を示す。

event volatility - イベントボラティリティ

Volatility driven by specific events, such as earnings announcements, that are expected to cause significant changes in stock prices.

決算発表などの、株価が大きく変動することが予想されるようなイベントによるボラティリティ。

EWMA model - 指数型加重移動平均モデル

The Exponentially Weighted Moving Average (EWMA) model estimates volatility based on past returns, assigning exponentially decreasing weights to older observations.

過去のリターンに基づいてボラティリティを推定するモデルで、古い観測値には指数的に小さな重みが与えられる。

ex-dividend - 配当落ち

The price at which the underlying asset of an option may be bought or sold when the option is exercised.

Non-standard options with more complex features than plain vanilla options.

バニラオプションとは異なり、より複雑な仕組みや条件を持つ非標準的なオプション。

A type of exotic option whose payoff depends on whether the underlying asset reaches or exceeds a specified barrier level during a certain period.

行使価格とは別にあらかじめバリア価格が設定されており、原資産が満期までの期間中にそのバリア価格に到達するかどうかによって、オプションが有効または無効になるタイプのエキゾチック・オプション。

contingent premium option - コンティンジェント・プレミアム・オプション

A type of exotic option that requires no premium upfront and only requires the buyer to pay a pre-specified premium if the option is in the money at expiration.

最初にプレミアムを支払う必要がなく、満期時にインザマネーになった場合にのみ、所定のプレミアムを支払うエキゾチック・オプションの一種。

A type of exotic option where the underlying is denominated in one currency, but the strike or payout is in another currency.

quanto option - クォント・オプション

A type of composite option in which the foreign exchange rate is fixed, eliminating currency risk for the investor.

コンポジット・オプションの一種で、為替レートが固定されているため、投資家にとって為替リスクを排除できる。

look-back option - ルックバックオプション

- Payout look-back options: A type of exotic option whose payoff is based on the most favorable observed price of the underlying asset during the life of the option (the maximum price for a call, the minimum price for a put).

- Strike-reset options (sometimes called reset look-backs): A type of exotic option in which the strike price is set at the end of a reset period to the least favorable level for the investor. For example, in a call, the strike is set to the highest underlying price observed during the reset period; in a put, the strike is set to the lowest. They are often cheaper than comparable vanilla ATM options because the strike adjustment removes the early-move benefit.

An exotic option whose value depends not only on the price of the underlying asset at maturity but also on the path the asset's price takes during all or part of the option's life.

満期時点の価格だけでなく、期間中の原資産の価格の動き(道筋)にも依存して価値が決まるエキゾチックオプション。

outperformance option - アウトパフォーマンス・オプション

A type of exotic option where the investor benefits if one underlying asset outperforms another underlying asset.

ある特定の原資産が別の原資産をアウトパフォームした場合に利益が発生するエキゾチック・オプションの一種。

worst-of option / best-of option - ワースト・オブ・オプション/ベスト・オブ・オプション

A worst-of option is a type of exotic option whose payoff is determined by the worst-performing underlying asset in a predefined basket, typically the one with the lowest value relative to the strike price at maturity.

Conversely, a best-of option refers to the corresponding structure where the payoff is determined by the best-performing asset in the basket, i.e., the one with the highest value relative to the strike.

Both worst-of and best-of options can be structured as calls or puts.

ワースト・オブ・オプションは、複数の原資産を参照するエキゾチック・オプションの一種であり、満期日にあらかじめ定められたバスケットの中で最もパフォーマンスが悪い原資産(権利行使価格に対して最も低い価値を示す資産)に基づいてペイオフが決まる。

これに対し、ベスト・オブ・オプションは最もパフォーマンスが良い原資産(権利行使価格に対して最も高い価値を示す資産)に基づいてペイオフが決まる。

The price at which an asset would be exchanged between a willing buyer and a willing seller in an orderly transaction at the measurement date.

公正価値とは、測定日において、合意した買い手と売り手の間で秩序ある取引により資産が交換される価格のこと。

gap risk - ギャップ・リスク

The risk that the price of an underlying asset will move significantly from its previous closing price, usually due to unexpected news or events occurring while the market is closed. This can result in a "gap" between the prior close and the next opening price.

原資産の価格が前日の終値から大きく乖離して動くリスク。通常、市場が閉まっている間に予期しないニュースや出来事が発生することが原因で、次の取引開始時にギャップが生じる。

inter-dealer - インターディーラーブローカー

far out of the money - ファーアウトオブザマネー

Describes an option whose strike price is significantly far from the current market price of the underlying asset, making it highly unlikely to be exercised profitably.

原資産の現在価格とかけ離れた行使価格を持ち、行使される可能性が極めて低いため、実質的な価値がほとんどないオプションの状態。

fill or kill/FOK - 一括執行注文(FOK注文)

An order that instructs a brokerage to execute the entire quantity of a transaction immediately; if it cannot be filled in full at once, it is canceled.

注文の全数量が直ちに約定できない場合には、すべてを失効させる一括執行の注文。

flat - 中立(フラット)

Flat means the net exposure in a particular risk factor is (approximately) zero due to hedging. Examples include gamma-flat, vega-flat, and theta-flat.

ヘッジによって特定のリスク要因に対する正味のエクスポージャーが(おおむね)ゼロになっている状態。例:ガンマ中立、ベガ中立、セータ中立。

Flexible Exchange Option (FLEX) - フレックス・オプション取引

Nonstandard, exchange-traded options that allow both the buyer and seller to customize key contract terms. These include the exercise style, strike price, expiration date, and other features such as settlement type.

権利行使方式、権利行使価格、満期、決済方式などの契約条件を、買い手と売り手が柔軟に設定できる非標準の取引所上場オプション。

The area of a securities exchange reserved for traders to buy and sell securities.

証券取引所においてトレーダーが売買を行うための専用エリア。

A bilateral agreement to buy or sell a specific asset at a predetermined price on a specified future date.

It is typically not traded on an exchange (i.e., it's an over-the-counter (OTC) contract).

先渡し契約とは、将来の特定の日に、あらかじめ定められた価格で特定の資産を売買する相対取引。取引所を通さず、当事者間で直接締結される店頭取引となる。

Forward Implied Volatility - フォワード・インプライド・ボラティリティ

The implied volatility for a future period (e.g., from T₁ to T₂), rather than from today to expiration. It can be derived from the implied volatilities at two different maturities on the term structure.

現在から満期までのインプライド・ボラティリティではなく、将来のある期間(例:将来の時点T₁から時点T₂まで)に対応するインプライド・ボラティリティ。ボラティリティの期間構造における、2つの異なる満期(現在からT₁までと、現在からT₂まで)のインプライド・ボラティリティから算出される。

forward price - 先渡し価格

forward start option - フォワード・スタート・オプション

An option that becomes effective on a specified future date, while the expiration date is determined at the time of purchase.

将来の特定日に発効するオプションで、満期日は購入時にあらかじめ設定されている。

forward volatility - フォワードボラティリティ

A measure of the implied volatility expected over a specific future period, derived from the term structure of volatility.

ボラティリティの期間構造から導かれる、将来の特定期間に予想されるインプライド・ボラティリティ。

The expected volatility of an option from the current time until its expiration. Traders estimate future volatility by analyzing historical volatility and using models such as ARCH, GARCH, or other related models.

オプションが現時点から満期までの期間において示すと予想されるボラティリティ。トレーダーは、ヒストリカルボラティリティを分析し、ARCH や GARCH などのモデルを用いてフューチャー・ボラティリティを推定する。

The rate of change in an option's delta with respect to a $1 change in the price of the underlying asset. Gamma is highest when the option is at-the-money.

原資産の価格が1ドル変動したときに、オプションのデルタがどれだけ変化するかを示す指標。アット・ザ・マネーのときに最も大きくなる。

gamma scalping - ガンマ・スキャルピング

A trading strategy that seeks to profit from price fluctuations of the underlying asset by dynamically adjusting a delta-neutral options position. It is typically used when implied volatility is low and expected to increase, or when actual price movement (realized volatility) is high enough to offset the time decay (theta) of the options.

For example, a trader might buy both a call and a put (a long straddle), creating a position with positive gamma. To keep the overall position delta-neutral, the trader buys or sells the underlying asset in response to price movements:

- If the price of the underlying rises, the trader sells some of the underlying to reduce delta.

- If the price falls, the trader buys the underlying.

Through this process, the trader effectively buys low and sells high, capturing small profits from price swings. However, the strategy is only profitable if the gains from these adjustments exceed the cost of the options' premiums and time decay.

原資産の価格変動(ボラティリティ)を利用して利益を狙うトレーディング戦略で、デルタ・ニュートラルなポジションを動的に調整することで実現される。一般的に、インプライド・ボラティリティ(IV)が低く、将来的に高まると予想される場合や、実現ボラティリティ(実際の価格変動)がオプションの時間的価値(セータ)の減少を上回ると見込まれる場合に用いられる。

たとえば、トレーダーがコールとプットの両方を購入することで(ストラドルの買い)、ガンマがプラスのポジションを構築する。この状態でポジション全体のデルタがゼロになるように、原資産を売買して調整する。

- 原資産価格が上昇すれば、デルタを中立に保つために原資産を売る。

- 原資産価格が下落すれば、原資産を買い増す。

このようにして、安く買って高く売ることを繰り返し、価格の上下動から小さな利益を積み重ねていく。ただし、オプションのプレミアム(購入コスト)やセータによる損失を上回る実現ボラティリティが必要であるため、すべての状況で利益が出るわけではない。

Generalized Autoregressive Conditional Heteroskedasticity. The GARCH model is an extension of the ARCH model that incorporates both past error terms and past variances to better capture long-term patterns in volatility.

GARCHモデルは、ARCHモデルを拡張したもので、過去の誤差項と分散の両方を取り入れることで、より長期的なボラティリティの変動パターンを捉えようとするモデル。

Good 'Til Canceled (GTC) - グッド・ティル・キャンセル(GTC)

A type of order to buy or sell a security that remains active until it is either executed in the market or canceled by the investor.

市場で約定するか、投資家がキャンセルするまで一定期間有効な買付または売却注文。

Financial measures of the sensitivity of an option's price to various parameters, such as the price of the underlying asset, time to maturity, volatility, and interest rates. These measures include delta, gamma, theta, vega, rho, and second-order Greeks such as vanna.

原資産価格、満期までの時間、ボラティリティ、金利などの要因に対して、オプション価格がどの程度変動するかを示す指標。グリークには、デルタ、ガンマ、セータ、ベガ、ローなどがあり、ヴァンナのような2次グリークも含まれる。

haircut - ヘアカット

hedger - ヘッジャー

The actual volatility of the underlying asset over a past period. Same as "realized volatility."

原資産の過去の一定期間における実際の変動率。「Realized volatility(実現ボラティリティ)」と同義。

Immediate or Cancel (IOC) - 未執行分取消条件付即時執行注文(IOC注文)

An order to buy or sell a security that will execute all or part immediately and then cancel any unfilled portion of the order.

指定した値段かそれよりも有利な値段で、即座に一部あるいは全部を約定させ、成立しなかった注文数量はキャンセルされる注文方法。

The level of volatility in an option’s underlying asset implied by the option’s current market price, as determined using a specific option pricing model. This value is typically obtained through iterative computation.

市場で実際に取引されているオプションプレミアムと、他の5つのパラメータから算出される、市場が織り込んでいるボラティリティ。コンピュータによる反復計算によって求められる。

index arbitrage - 指数裁定取引

initial margin - 当初証拠金

intraday margin - 日中証拠金

A situation where an option has intrinsic value — that is, the price of the underlying asset is favorable relative to the strike price, so exercising the option at that point in time would result in a profit.

intremarket spread - 市場間スプレッド

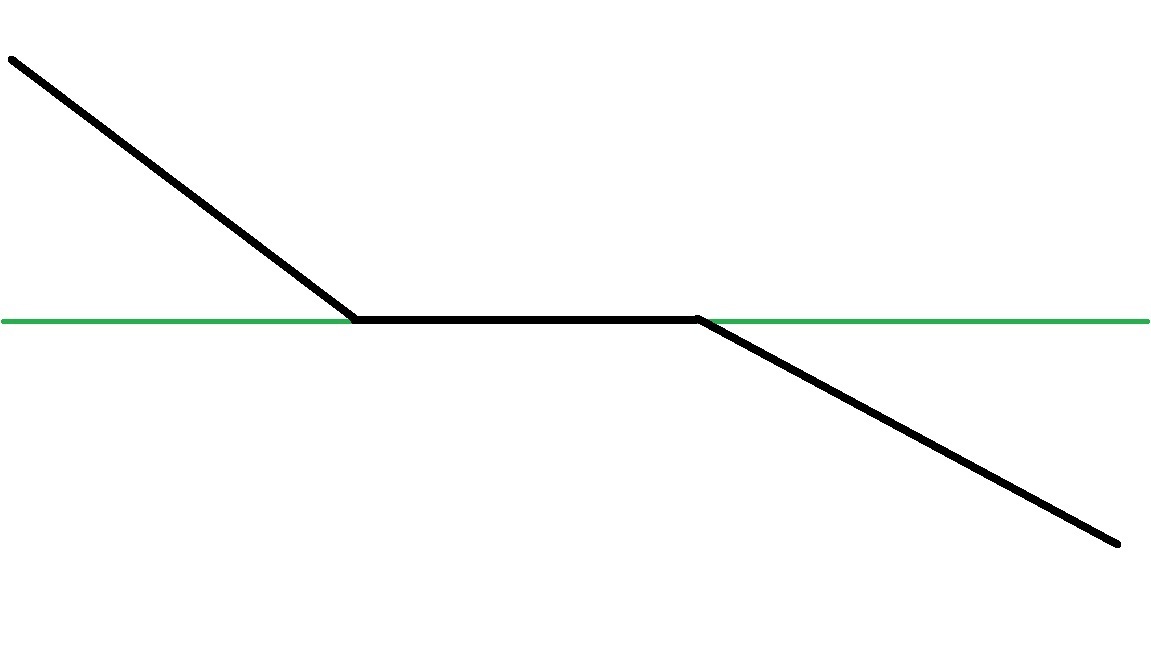

iron condor - コンドル

A strategy in which a bull put spread and a bear call spread are sold simultaneously, using four strike prices. The short put spread is opened at lower strikes, while the short call spread is opened at higher strikes.

4つの異なる行使価格を用いて、ブルプットスプレッドとベアコールスプレッドを同時に売る戦略。プットスプレッドは低い行使価格、コールスプレッドは高い行使価格で構築される。

jelly roll - ジェリーロール

A strategy in which a synthetic short position (short combo) is established in the near-term expiration, and a synthetic long position (long combo) is established in the longer-term expiration, both at the same strike price. It is typically used when there is an expectation regarding future dividends or interest rates. Also called a “roll.”

近い満期でショートコンボ(合成ショート)を構築し、遠い満期でロングコンボ(合成ロング)を構築する戦略。 行使価格は同じ。将来の配当や金利についての見通しがある場合に活用される。別名「ロール」。

Kappa - カッパ

knock-in option - ノックインオプション

An option contract that only becomes active if the underlying asset reaches a predetermined price level before expiration.

原資産が満期前に、あらかじめ定められた価格に到達した場合にのみ、有効となるオプション。

knock-out option - ノックアウトオプション

An option contract that expires worthless if the underlying asset reaches a specified price level before expiration.

原資産が満期前に、あらかじめ定められた価格に到達すると、無効となるオプション。

kurtosis - 尖度(カートシス)

Kurtosis is a statistical measure that describes the degree of tailedness in a probability distribution — that is, how heavy or light the tails are compared to a normal distribution.

正規分布との比較における、確率分布の裾の重さ(太さ)を示す統計量。

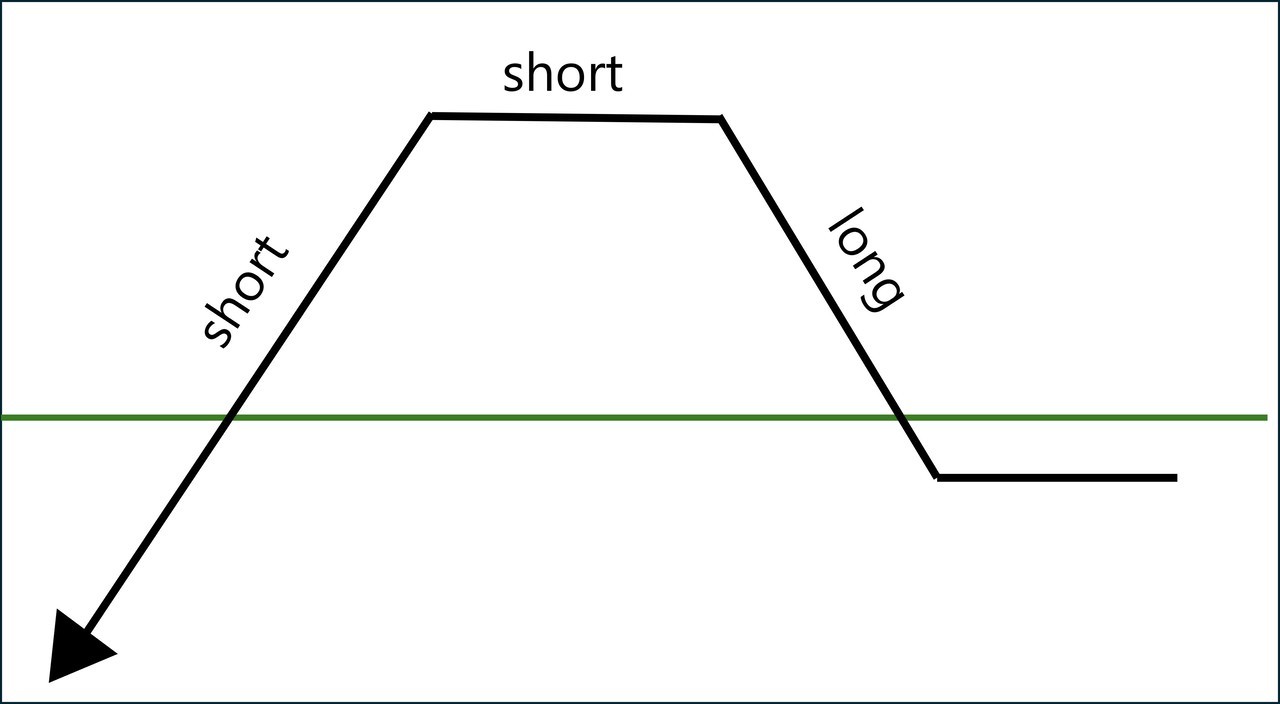

ladder (strategy) - ラダー(戦略)

A strategy that involves combining three options of the same type (all calls or all puts) with three different strike prices,

同じタイプ(すべてコールまたはすべてプット)のオプションを、異なる3つの行使価格で組み合わせる戦略。

ladder option - ラダーオプション

An option that locks in incremental profits as the underlying asset reaches predetermined price levels. The more levels the asset reaches, the more profit is secured, regardless of whether it later falls below those levels.

原資産があらかじめ設定された段階的な価格水準に達するたびに、利益が順次確定していくオプション。達成した価格水準を下回っても、その時点で確定した利益は維持される。

A single component or contract within a multi-contract trading strategy. For example, a butterfly spread consists of three legs.

複数の契約で構成されるトレーディング戦略における個々の契約(構成要素)のこと。たとえば、バタフライ・スプレッドには3つのレッグが含まれる。

limit - リミット

An order to buy or sell at a specific price or better. A buy limit order will only be executed at the limit price or lower, and a sell limit order at the limit price or higher.

あらかじめ指定した価格、またはそれより有利な価格で、売買する注文。買い注文の場合はその価格以下、売り注文の場合はその価格以上でのみ執行される。

locked market - ロックト・マーケット

A market condition in which the best bid and best ask prices for a security are equal, typically occurring temporarily due to order flow or latency.

取引所において、最良買い気配と最良売り気配が一時的に同じ価格になる状態。主に注文のタイミングやシステムの遅延などにより発生する。

logarithmic return - 対数リターン

Logarithmic return (also known as log return) is defined as: ln(Present Value / Past Value). It measures the continuous rate of return of an asset and accounts for the compounding effect over time.

ln(現在の原資産価格 ÷ 過去の原資産価格)。時間の経過に伴う複利効果を考慮し、資産の連続的な収益率を測定する方法。

Long-Term Equity Anticipation Security (LEAPS) - 株式長期オプション(LEAPS)

An option with an expiration date longer than one year, typically up to three years.

満期までの期間が1年以上ある株式オプション。最長で3年となる。

maintenance margin - 維持証拠金

Collateral required to open or maintain a position, such as buying the underlying asset or entering into option transactions. Margin refers to cash or other assets deposited by traders or institutional investors with brokers or clearinghouses to cover potential losses or meet margin requirements.

ポジションを新規に建てたり維持したりするために必要な担保。トレーダーや機関投資家が、損失の可能性をカバーしたり、証拠金要件を満たしたりする目的で、証券会社や清算機関に差し入れる現金またはその他の資産を指す。顧客が証券会社に預ける証拠金は「委託証拠金」と呼ばれる。

margin call - マージンコール

market-if-touched (MIT) order - 条件付き成り行き注文(MIT)

A conditional order that becomes a market order to buy or sell once a specified price level is touched, even if only briefly.

証券が指定した価格に達したときに、成行注文として発動される条件付き注文。

market maker - マーケットメイカー

market not held order - マーケット・ノットヘルド・オーダー

Market-on-Close (MOC) order - 引成注文

A type of market order that is executed at or near the market close, at the closing price. It ensures execution, but the final price may be affected by end-of-day volatility.

引けのタイミングで成行注文として執行される注文。必ず執行されるが、終盤の価格変動による影響を受ける可能性がある。

An order placed by an investor to buy or sell assets immediately at the best available price in the current market.

価格を指定せず、市場の実勢価格で直ちに執行される注文。

mark-to-model - マーク・トゥ・モデル

A method used to estimate the value of illiquid or infrequently traded financial instruments based on internal pricing models rather than observable market prices.

市場で頻繁に取引されない、流動性の低い金融商品の価値を、市場価格ではなく社内の価格モデルに基づいて見積もる方法。

married put - マリードプット

An options strategy in which an investor simultaneously purchases a put option and the underlying asset. A married put is similar to a protective put, but the key distinction is that the put and the underlying asset are bought at the same time.

原資産とプットオプションを同時に購入し、原資産の価格下落リスクをヘッジする戦略。プロテクティブプットと似ているが、両者の違いはプットと原資産を同時に買う点にある。

multiplier - マルティプライア

The number of units of the underlying asset that one option contract represents.

1つのオプション契約が、いくつの原資産に対応しているかを示す数値。

naked option - ネイキッドオプション

naked put - ネイキッド・プット

A strategy in which the investor writes (sells) put options without holding a short position in the underlying asset and without setting aside the cash to buy the underlying asset if assigned. Also called an “uncovered put,” “short put,” or “put underwriting.”

プットを売る戦略のひとつであり、同時に原資産の空売りしておらず、オプションが行使された場合に原資産を購入するための現金も確保していないもの。「裸のプット売り」とも呼ばれる。

A situation where the option’s strike price is close to the current market price of the underlying asset.

notional - 名目元本(ノーショナル)

Volatility swap: The notional (volatility notional) is the dollar amount per 1% change in volatility and is negotiated between the counterparties.

Variance swap: The notional (variance notional) is typically set so that the variance swap has the same vega as a volatility swap; it is calculated as the volatility notional divided by 2σS, where σS is the strike volatility.

ボラティリティ・スワップの場合:名目元本は、ボラティリティ1%の変化による損益額を表し、取引相手間で交渉されます。

バリアンス・スワップ(分散スワップ)の場合:多くの場合、名目元本は同じベガを持つボラティリティ・スワップの名目元本を2σS(ストライク・ボラティリティ)で割った値として設定されます。

notional value - 名目価値

The notional value represents the total nominal size of a position, commonly used in derivatives. It is typically calculated by multiplying the number of contracts by the size of the underlying asset and its current (spot) price. It gives a sense of the scale or exposure of the position, even though the actual amount exchanged may differ.

デリバティブ取引において、ポジションの名目上の規模を示す金額。通常、契約数量に原資産の単位数と現在の価格(スポット価格)を掛けて算出され、実際にやり取りされる金額とは異なる場合があるが、ポジションの大きさを把握するために用いられる。

OCC - オプション・クリアリング・コーポレーション(OCC)

The largest clearing organization in the U.S. specializing in listed equity options. It acts as a central counterparty and guarantees the settlement of trades.

米国の株式デリバティブ専門の清算機関。売買の相手方に代わり、証券の受渡しと決済代金の受払いにかかる債務を引き受け、決済の履行を保証する。

offer - オファー

One Cancel the Other (OCO) - OCO注文(二者択一注文)

A pair of conditional orders placed simultaneously. When one of the orders is executed, the other is automatically canceled.

2つの条件付き注文を同時に発注し、どちらか一方の注文が執行されると、もう一方の注文が自動的にキャンセルされる。

open interest - オープンインタレスト

The total number of outstanding (unsettled) contracts in options or futures markets that have not been closed or delivered.

オプションや先物市場で、未決済のまま残っている契約(建玉)の総数。

The flow of buy and sell orders submitted by traders and institutional investors in the market.

オーダーフローとは、トレーダーや機関投資家が市場に出す売買注文の流れを指します。

A situation where the option would have no intrinsic value if it were maturing now.

もし今が満期であればオプションに本質的価値がない状態。

You already hold the underlying position and sell an option on it to earn premium income, usually because the option appears overpriced.

原資産をすでに保有しており、その原資産を対象とするオプションが割高と判断される場合、オプションを売ってプレミアムを得ること。

A condition where the price of an option is equal to its intrinsic value, typically meaning there is no time value.

physical settlement - 現物決済

The process of settling a contract by delivering the actual underlying asset, such as stocks or commodities, from the seller to the buyer.

対象となる原資産(株式や商品など)を実際に受け渡すことで行う決済方式。

position limit - 建玉制限

The price paid by the buyer to the seller to acquire an option contract.

オプションの買い手が売り手に支払う、オプション契約の取得にかかる価格。

program trading - プログラム売買

The right, but not the obligation, to sell an underlying asset at a specified price within a specified period of time.

特定の原資産を、あらかじめ定められた価格で、あらかじめ定められた期日またはその期日までに売却できる権利。

put-call parity - プットコールパリティ

A principle that defines a specific relationship between the prices of European call and put options with the same strike price and expiration date, based on arbitrage logic.

A range forward is an foreign exchange hedging strategy typically used by exporters, where they buy a put option at a lower strike price and sell a call option at a higher strike price. The premiums received and paid are structured to exactly offset each other, making the strategy a zero-cost option.

輸出企業などが為替リスクをヘッジするために利用する戦略で、ある行使価格のプットを購入し、より高い行使価格のコールを売却することにより、一定のレートレンジを確保する。プットとコールのプレミアムは相殺され、実質的にコストがかからないゼロコストオプション戦略となっている。

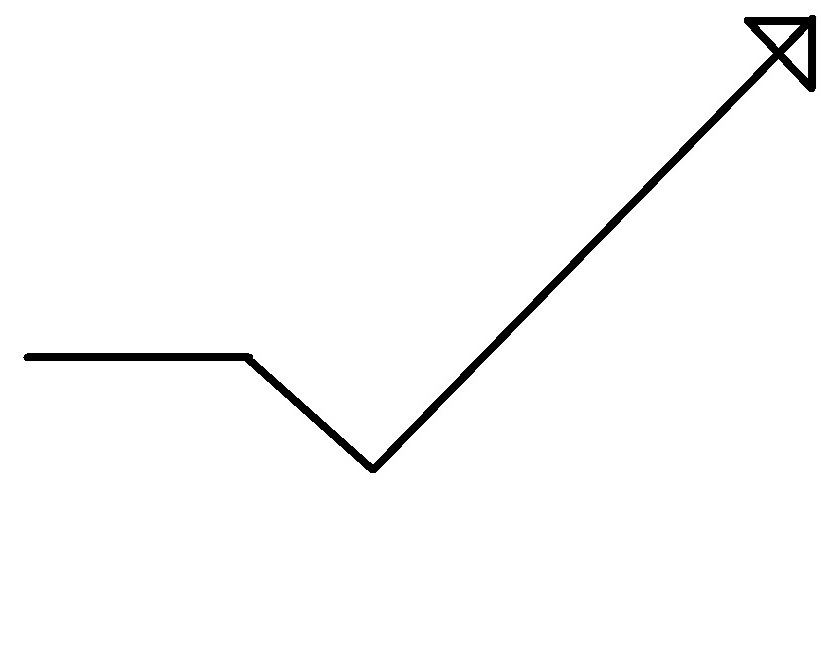

ratio backspread - レシオバックスプレッド

A directional options strategy that involves selling a smaller number of options at one strike price and buying a larger number of options at a different strike price, all with the same expiration date. The strategy profits from significant movement in the underlying asset, and may incur losses if the price stays within a narrow range.

同一満期のオプションにおいて、より少ない数のオプションをある権利行使価格で売り建て、異なる権利行使価格でより多くの数のオプションを購入する戦略。原資産価格が大きく動いた場合に利益が出る一方、価格の変動が狭い範囲にとどまる場合、損失が発生する可能性がある。

call ratio backspread - コールレシオバックスプレッド

put ratio backspread - プットレシオバックスプレッド

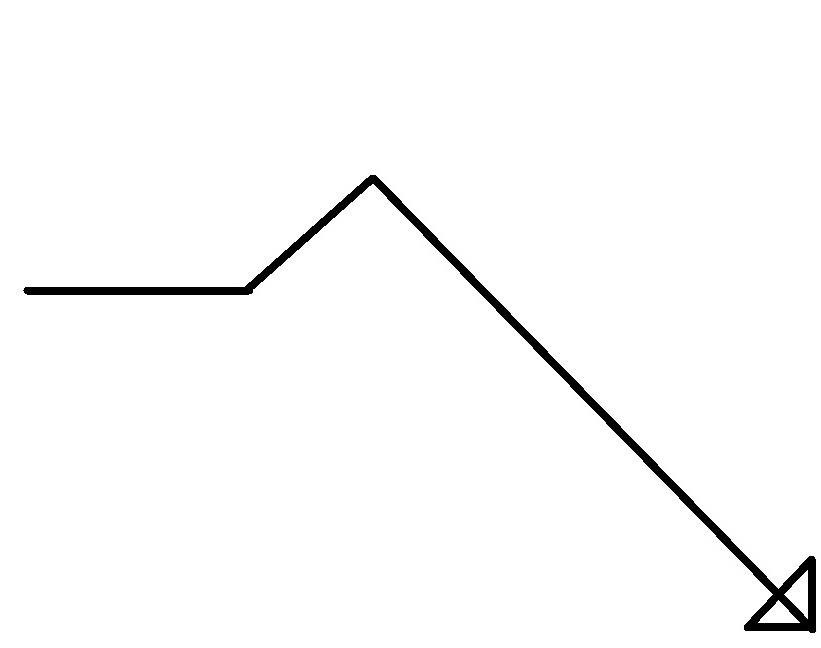

ratio spread - レシオスプレッド

A strategy that involves buying a certain number of options at one strike price and selling a greater number of options at a different strike price, all with the same expiration date. It is typically designed to result in a net credit (premium received), and can be used to express a moderately directional view.

オプションを買い、より多くのアウト・オブ・ザ・マネーのオプションを別の権利行使価格で売却する戦略。同一満期で構成され、プレミアムの差し引きでネットクレジット(受け取り)を得ることを目的とする。

call ratio spread/ratio call spread - コールレシオスプレッド/レシオコールスプレッド

A strategy that involves buying one call option at a lower strike price and selling a greater number of call options at a higher strike price. The strategy is designed to earn a net premium and profits if the underlying asset rises moderately, but may incur losses if the price rises significantly beyond the higher strike.

権利行使価格の低いコールを1枚購入し、より高い行使価格のコールを複数枚売り建てる戦略。プレミアムの差し引きによりネットで受け取りが発生する。原資産価格が適度に上昇した場合に利益が得られるが、急騰した場合には損失が発生する可能性がある。

put ratio spread/ratio put spread - プットレシオスプレッド/レシオプットスプレッド

A strategy that involves buying one put option at a higher strike price and selling a greater number of put options at a lower strike price. The strategy is designed to earn a net premium and profits if the underlying asset falls moderately, but may incur losses if the price drops significantly below the lower strike.

権利行使価格の高いプットを1枚購入し、より低い行使価格のプットを複数枚売り建てる戦略。プレミアムの差し引きによりネットで受け取りが発生する。原資産価格が適度に下落した場合に利益が得られるが、急落した場合には損失が発生する可能性がある。

ratio write - レシオライト

The actual volatility of an asset, calculated from historical price data over a specific period.

原資産の過去の価格変動に基づいて算出される実際のボラティリティ。

reverse conversion/reversal - 逆コンバージョン/リバーサル

The rate of change in an option’s price with respect to changes in the risk-free interest rate.

オプション価格の無リスク金利に関する偏微分係数(すなわち、金利の変化に対する価格の感応度)。

rights issue - 株主割当増資

An offer by a company to its existing shareholders to buy additional shares, typically at a discount to the current market price, and within a specified timeframe.

既存の株主に対して、市場価格よりも割安な価格で追加の株式を一定期間内に購入できる権利を付与するもの。

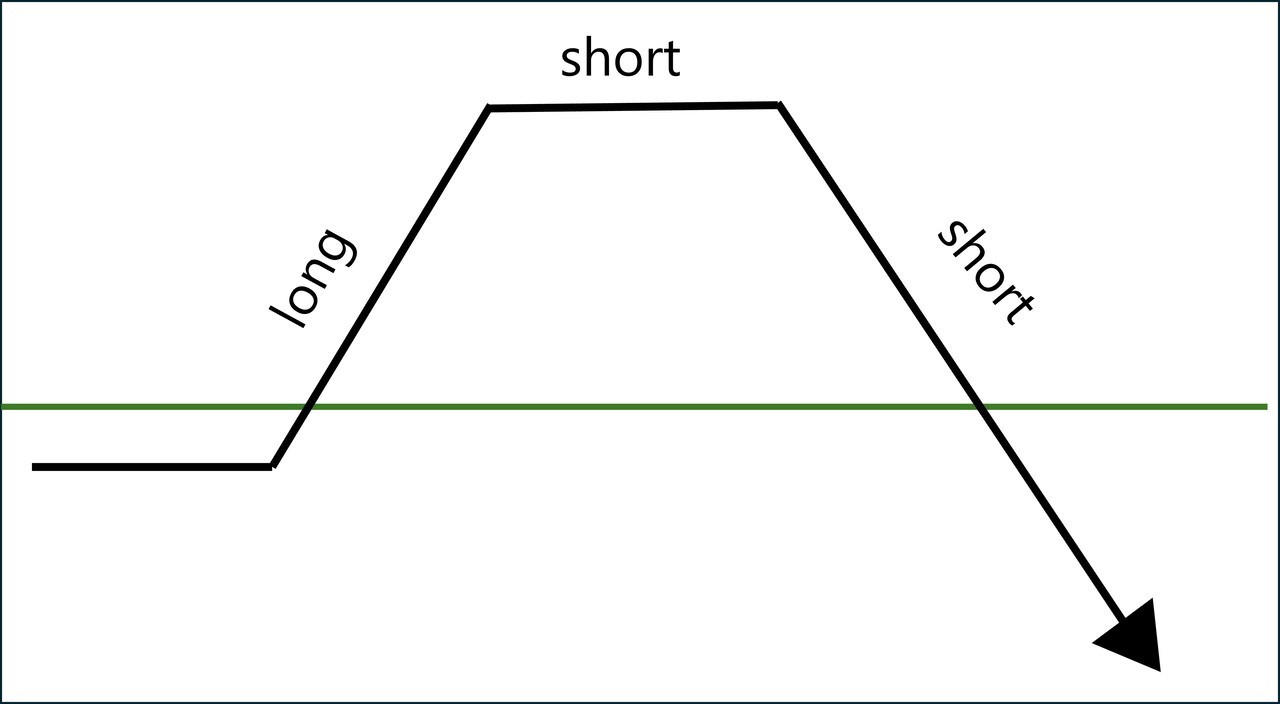

risk reversal - リスクリバーサル

A strategy involving the simultaneous purchase of an out-of-the-money option and sale of an out-of-the-money option in the opposite direction — either buying a put and selling a call, or vice versa. When a put is bought and a call is sold, the structure resembles a range forward; however, the purpose of a risk reversal is typically to express a directional market view rather than to hedge.

アウト・オブ・ザ・マネーのオプションの買い建てと売り立てを両方行う戦略で、プットを買ってコールを売る、またはその逆の組み合わせとなる。プットを買ってコールを売る場合、構造的にレンジフォワードに似ているが、リスクリバーサルは通常、ヘッジではなく、相場の方向性に対する見通しに基づいて利益を狙う目的で用いられる。

rolling - ローリング

An options adjustment strategy in which a trader closes an existing position and opens a new one with different terms. Common adjustments include changing to a higher strike price (roll up), a lower strike price (roll down), a later expiration date (roll forward), or a combination of these (roll up and out or roll down and out).

既存のポジションを解消し、条件が異なる別のオプションに乗り換える調整戦略。よくある調整としては、より高い行使価格への変更(ロールアップ)、より低い行使価格への変更(ロールダウン)、満期日をより後ろに延ばす変更(ロールフォワード)、あるいはそれらを組み合わせた調整(ロールアップ・アンド・アウトやロールダウン・アンド・アウト)などがある。

An options adjustment strategy in which a trader closes an existing position and opens a new one with a higher strike price, typically to lock in gains or adjust to market movements. It is the opposite of a roll down.

既存のポジションをクローズし、より高い行使価格のポジションを新たに建てる調整戦略。通常は利益確定や市場環境の変化に対応する目的で行われ、「ロールダウン」とは逆の方向の調整となる。

series - シリーズ

A group of options contracts of the same class (i.e., same underlying asset and type: call or put), with the same strike price and expiration date.

short squeeze - 踏み上げ

A sharp rise in the price of a stock, not due to fundamentals, but triggered by short sellers buying back shares to cover their positions. As the stock price unexpectedly increases, short sellers are forced to cover, which further drives the price up, creating a feedback loop.

株価がファンダメンタルズではなく、空売り投資家の買い戻しによって急騰する現象。株価が予想に反して上昇すると、空売り投資家は損失を抑えるために買い戻しを行い、それがさらなる株価上昇を招く。これにより、他の空売り投資家も買戻しを迫られ、連鎖的に株価が急騰する。

sigma - シグマ

A statistical measure that quantifies the degree of asymmetry in a probability distribution.

確率分布の非対称性を示す統計量。

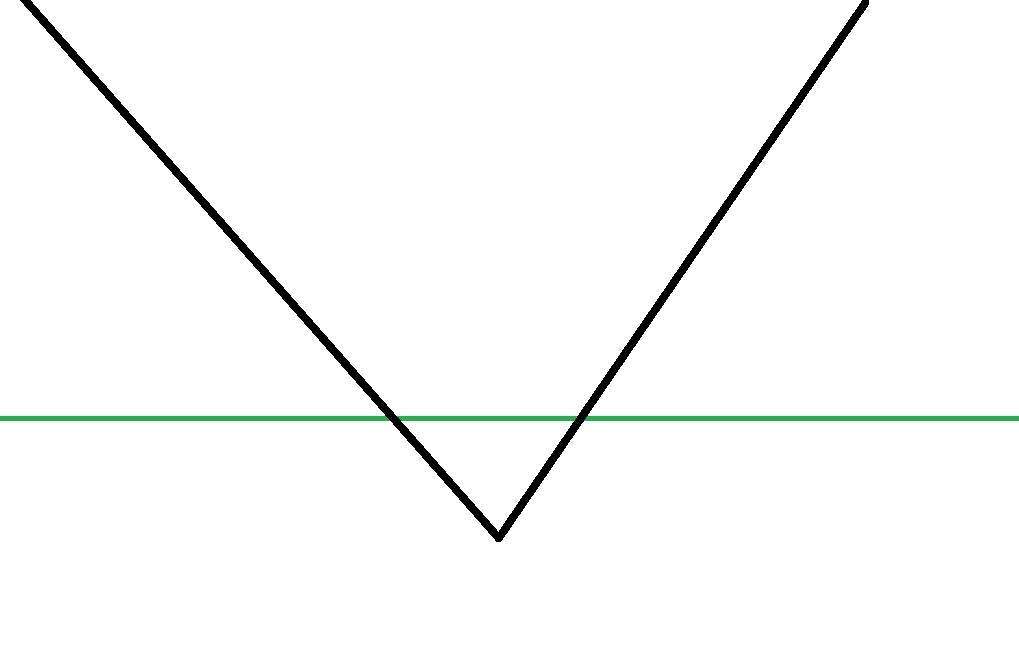

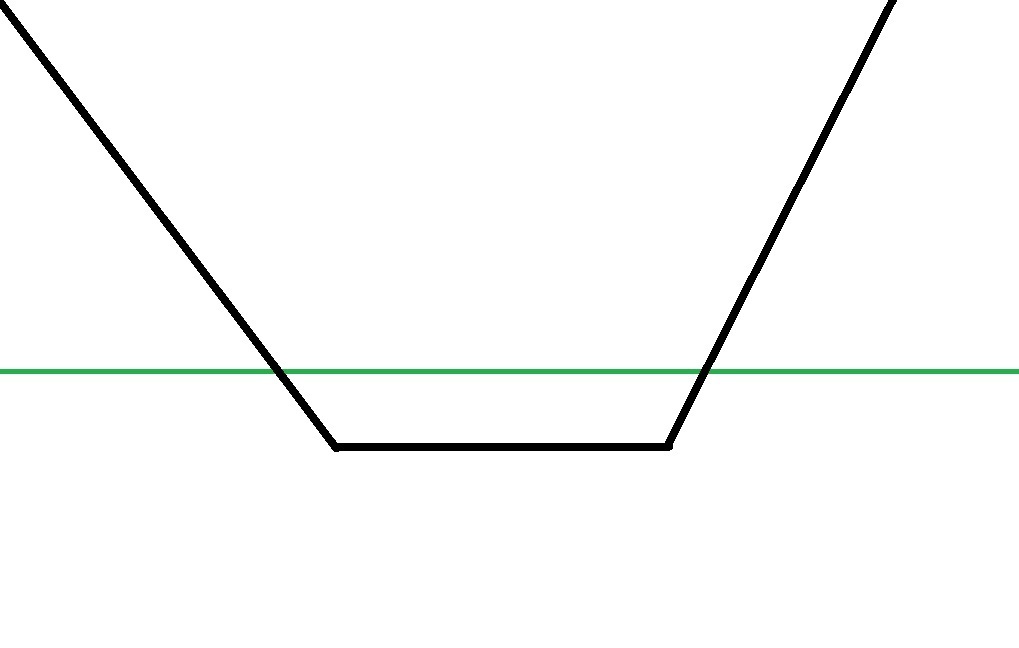

A volatility smirk refers to a pattern where implied volatility is significantly higher for deep out-of-the-money put options, resulting in an asymmetrical volatility curve.

遠いアウト・オブ・ザ・マネー(OTM)のプットオプションに対してインプライド・ボラティリティが高くなることで、ボラティリティカーブが非対称になる現象を指す。。詳細はこちら

softs - ソフトコモディティ

Commodities that are cultivated or raised, rather than extracted or mined.

栽培または飼育によって生産される商品(例:コーヒー、砂糖、綿花)で、農作物や家畜が含まれる。

Speed - スピード

A trading strategy that involves the simultaneous purchase and sale of two or more options (or other financial instruments) to limit risk or take advantage of price differences.

リスクを限定したり、価格差を活用したりすることを目的に、2つ以上のオプション(または他の金融商品)を同時に売買する取引戦略。

Spreads involving options with different strike prices, but with the same expiration date.

horizontal spread - ホリゾンタルスプレッド

Spreads involving options with the same strike price, but with different expiration dates. Also known as a time spread or calendar spread.

権利行使価格が同一で、満期日が異なるオプションによるスプレッド。「タイムスプレッド」または「カレンダースプレッド」とも呼ばれる。

stop order - ストップ注文(逆指値注文)

An order to buy a security once its price rises to a specified level, or to sell once its price falls to a specified level.

あらかじめ指定した価格まで株価が上昇した場合に買い、または下落した場合に売ることを予約する注文。

stop-limit order - ストップリミット注文

An order that is triggered when a specified stop price is reached, at which point it becomes a limit order to buy or sell at a specified limit price or better.

あらかじめ指定したストップ価格に達すると、指定した指値価格またはそれより有利な価格でのみ執行される指値注文に変わる注文。

long straddle

A straddle is a strategy in which an investor holds both a call option and a put option with the same strike price and expiration date on the same underlying asset.

同じ原資産に対して、同じ行使価格・同じ満期のコールオプションとプットオプションを1つずつ買う(ロング・ストラドル)または売る(ショート・ストラドル)戦略。

straddle swap - ストラドルスワップ

A long straddle swap (also called a calendar straddle swap) involves buying a longer-dated (back-month) straddle and selling a shorter-dated (front-month) straddle, using the same strike price and underlying asset.

同じ原資産・同じ行使価格で、満期の遠いストラドルを買い、満期の近いストラドルを売る取引(ロングの場合)。カレンダー・ストラドルスワップとも呼ばれる。

strangle - ストラングル

long strangle

A strategy in which an investor buys (long) or sells (short) both a call and a put with different strike prices but the same expiration date, on the same underlying asset.

同じ原資産・同じ満期で、異なる行使価格のコールとプットを1つずつ買う(ロング・ストラングル)または売る(ショート・ストラングル)戦略。

The price at which the holder of an option can buy or sell the underlying asset.

オプションが行使されたときに原資産の売買を行う価格。

stub trade - スタブ取引

A relative value strategy in which a trader compares the market value of a parent company with the value of its subsidiaries (or other holdings) to isolate the value of the parent’s remaining assets — the “stub.” The trade typically involves long–short positions to exploit perceived mispricing between the parent and its holdings.

レラティブ・バリュー戦略の一種で、トレーダーは親会社の時価とその子会社(またはその他の保有資産)の価値を比較することにより、親会社の残りの資産(スタブ部分)の価値を分離する。ロング・ショートのポジションを取ることが多く、親会社とその保有資産のミスプライシングから利益を得ることを狙う。

ちなみに、「スタブ」とは英語で、木の切り株や映画・乗り物のチケットの半券を指し、「何かを切り取った後に残った部分」という意味がある。

synthetic call - 合成コール

synthetic put - 合成プット

tail risk - テイルリスク

The risk of extremely rare events that lie in the "tails" of a probability distribution.

確率分布の「裾(テイル)」に位置する、極めてまれな事象が発生した際に生じるリスク。例えば、3標準偏差を超えるような非常に低い確率でしか起こらない事象。

A way of illustrating the relationship between the implied volatilities of options with different expiration dates on the same underlying, helping to understand how the market perceives the underlying's future volatility over time.

インプライドボラティリティの満期に対する変化の様子。

An option's time decay—the rate at which the value of an option decreases with the passage of time, assuming all other factors remain constant.

時間の経過によってオプションの価値が減少する度合い(タイムディケイ/1日あたりの減少分)を示す指標。

Theta-weighted pair trade - インプライド・ボラティリティーの変化率で加重するペアトレード

In this type of trade, a trader goes long the implied volatility of one underlying asset and hedges the position by shorting the implied volatility of another underlying asset, sizing the positions under the assumption that the implied volatilities of both assets will move by the same percentage.

The trader will profit if the implied volatility of the long position rises (or falls less) relative to the implied volatility of the shorted position, compared with the proportional move assumed when sizing the hedge.

Here, the word “theta” does not refer to time decay.

ある原資産のインプライド・ボラティリティをロング、別の原資産のインプライド・ボラティリティをショートにしてヘッジするペアトレード。ポジションのサイズは、両資産のインプライド・ボラティリティが同じ割合で変動すると仮定して決定される。

ロングのポジションのインプライド・ボラティリティがショートのポジションのインプライド・ボラティリティよりも、実際に相対的に上昇(または下落幅が小さい)した場合、利益を得られる。

英語で「Theta」と呼んでいるものの、ここでは時間価値の減少(タイムデケイ)を意味するものでないため、注意が必要。

The value of an option derived from the expectation that the underlying asset will fluctuate before maturity.

原資産が満期までに変動すると期待されることに由来するオプションの価値。

The financial instrument or asset on which an option contract is based.

オプション契約において、権利行使の対象となる基礎資産。

The specific security on which an option contract is based.

オプションにおいて、権利行使の対象となる基礎となる証券。

underlying stock - 対象株式

Vanna is the rate of change of delta with respect to implied volatility, and equivalently, the rate of change of vega with respect to the price of the underlying asset.

インプライド・ボラティリティの変化によってデルタがどのように変化するか、また原資産価格の変化によってベガがどのように変化するかを示す指標。デルタをインプライド・ボラティリティで偏微分したものであり、または、ベガを原資産価格で偏微分したものでもある。

[Reference 参考]

The statistical measure of how much the return (typically log return) of an underlying asset deviates from its expected value over a given period of time; it is the square of the standard deviation.

原資産の連続複利リターン(対数リターン)が期待値からどれだけ乖離するかを示す統計量で、標準偏差の二乗。

variance future - バリアンス先物

A forward contract structured as a swap in which one leg reflects the realized variance of an asset over a specified period, and the other leg reflects a fixed strike variance. At maturity, the contract is settled in cash based on the difference between the two, multiplied by the notional amount.

資産の一定期間における実現バリアンスと、あらかじめ定められたストライクバリアンスとの差に基づいて損益が決まり、名目元本を乗じた金額が差金決済されるスワップ契約。

corridor variance swap - コリドー・バリアンス・スワップ

A type of variance swap where the realized variance is calculated using only the observed prices that are within a predetermined range (the corridor).

原資産の価格があらかじめ定められた一定範囲(コリドー/回廊)内にある間の値動きのみを用いて実現分散を算出するスワップ。

down variance swap - ダウン・バリアンス・スワップ

A type of corridor variance swap where the upper bound of the corridor is the current spot when the trade is initiated.

コリドー・バリアンス・スワップの一種で、コリドーの上限が取引開始時のスポット価格となるもの。

up variance swap - アップ・バリアンス・スワップ

A type of corridor variance swap where the lower bound of the corridor is the current spot when the trade is initiated.

コリドー・バリアンス・スワップの一種で、コリドーの下限が取引開始時のスポット価格となるもの。

variation margin - 変動証拠金

A payment made to or received from a clearinghouse to reflect changes in the market value of a position.

The amount an option's price is expected to change for a 1% change in implied volatility.

インプライドボラティリティが1ポイント上昇したときにオプションの価値がどれほど上昇するかを表した指標。

VIX - 恐怖指数(VIX)

Volatility Index. A measure of the stock market's expectation of 30-day volatility based on S&P 500 index options. Also known as the market's “fear index.”

S&P500指数の今後30日間のインプライド・ボラティリティを示す指標。

The standard deviation of the continuously compounded annual returns of the underlying asset.

原資産の連続複利リターン(年率換算)の標準偏差。

volatility carry - ボラティリティ・キャリー

The potential profit from holding a volatility position, usually earned by selling options when implied volatility exceeds realized volatility. It is independent of the underlying's price direction and reflects the spread between implied and realized volatilities.

Implied volatility is often higher than realized volatility because options reflect market fear and are commonly used for insurance purposes.

オプションを売り、インプライド・ボラティリティが実現ボラティリティを上回る場合に得られる利益。原資産の価格の方向性には影響されない。インプライド・ボラティリティと実現ボラティリティの差分が利益となる。オプションは市場の恐怖心理を反映し、保険目的で利用されることが多いため、インプライド・ボラティリティが実現ボラティリティを上回る傾向がある。外貨のキャリー取引における『キャリー』とは意味が異なる。

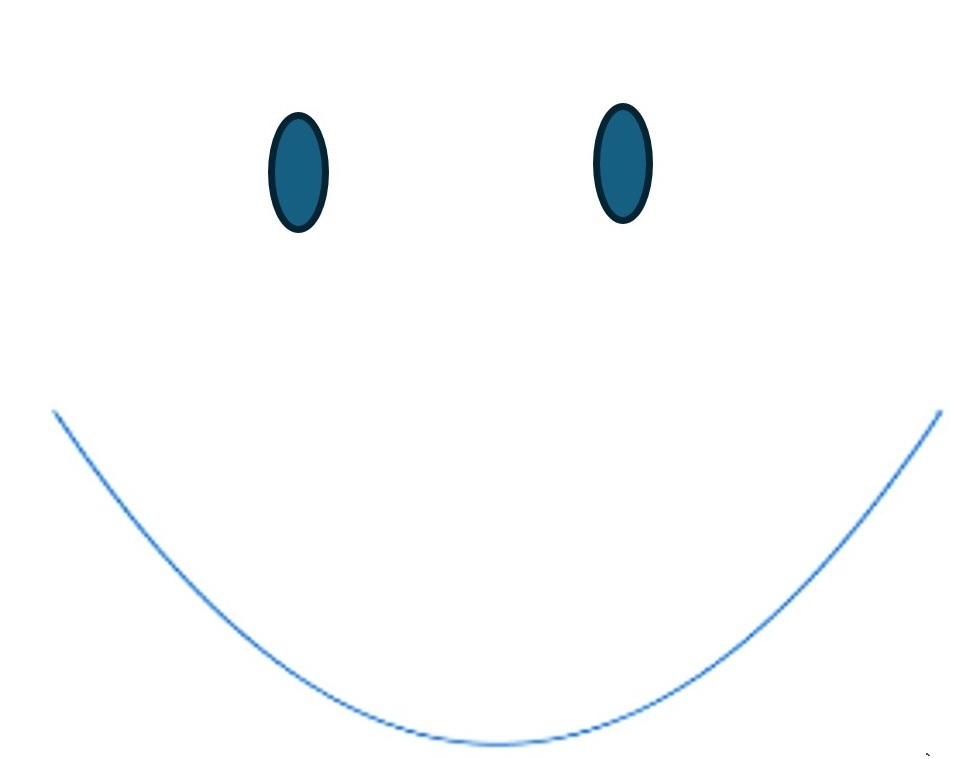

A volatility smile is a graph that shows implied volatility increasing as the option’s strike price moves away from being at-the-money, whether it becomes more in-the-money or out-of-the-money. This pattern forms a symmetrical curve, resembling a smile.

When the graph is asymmetrical—typically with implied volatility rising only as the strike price decreases (often for puts)—the pattern is referred to as a volatility smirk.

オプションの行使価格がアット・ザ・マネー(ATM)から離れ、よりイン・ザ・マネーまたはアウト・オブ・ザ・マネーになるにつれて、インプライド・ボラティリティが増加するという特性を表した図を「ボラティリティスマイル」と呼ぶ。このグラフは一般的に左右対称の形状をしており、笑顔のように見えることからその名がついています。

一方で、特にプットオプションで行使価格が低くなるほどインプライド・ボラティリティが上昇し、グラフが左右非対称になる場合は、「ボラティリティスマーク(smirk)」と呼ばれる。

volatility surface - ボラテイリティサーフィス

A three-dimensional graph that shows the implied volatility of options plotted against both the strike price and the time to maturity, for a given underlying asset. It captures patterns such as smiles, skews, or smirks depending on market conditions.

特定の原資産に対するオプションのインプライド・ボラティリティを、行使価格と満期までの期間の2軸に対してプロットした三次元のグラフ。市場環境に応じてスマイルや歪度、スマークなどさまざまなパターンが見られる。

volga - ボルガ

A second-order option Greek that measures the rate of change of vega (the sensitivity of an option’s price to changes in implied volatility) with respect to implied volatility. Also called Vomma.

ベガ(インプライドボラティリティの変化に対するオプション価格の感応度)をさらにインプライドボラティリティで偏微分したグリーク。「ボンマ」とも呼ばれる。

warrant - 新株予約権証券(ワラント)

A warrant is a security issued by a company that gives the holder the right, but not the obligation, to purchase newly issued shares of that company at a specified price (exercise price) within a defined period.

会社が発行する有価証券であり、所定の価格で一定期間内にその会社の新株を取得する権利(義務ではない)を投資家に与えるもの。

Reference - 参考:

Colin Bennett, (2014) "Trading Volatility, Correlation, Term Structure and Skew"

Dan Passarelli, (2012) "Trading Options Greeks: How Time, Volatility, and Other Pricing Factors Drive Profits," Bloomberg Press

Jon Spiegel, CFA, September 22, 2022, Calendar Collar Overlay, clarivor

Lawrence G. McMillan, (2012) "Study Guide for Options as a Strategic Investment," Prentice Hall Press

Sheldon Natenberg, (1994) "Option Volatility & Pricing: Advanced Trading Strategies and Techniques," McGraw-Hill

シェルダン・ネイテンバーグ, (2006)「オプションボラティリティ売買入門」 パンローリング

リチャードM. ブックステーバー, (1990) 「オプション価格と投資戦略」金融財政事情研究会

佐藤 茂, (2013)「実務家のためのオプション取引入門」ダイヤモンド社

翻訳のご用命は

当事務所の代表の木本です。

あなたのお悩みを解決します!

・オルタナティブ投資の分野は日々、新しいコンセプトが生まれており、その内容にふさわしい和訳が必要です。

・きもとオルタナティブ翻訳は、たとえ辞書に載っていない専門用語でも、意味を考えながら日本語にしております。

・翻訳にお困りの際は、ぜひお気軽にご相談ください。